June 22, 2021

By Roger Longman

The pharmaceutical industry faces a large and ugly problem: the growing economic burden on their payer customers of specialty drugs. As always with tangled problems, there is an increasingly popular Gordian Knot solution: slicing it through with the governmental sword of price controls. And those in favor of such solutions are not merely the political left: 50% of large employers think government should limit costs of expensive therapies[1]; a third of employers want it to negotiate prices or set limits on price increases.

The industry has countered with various arguments. That new drugs lower total health care costs by lowering hospital or caregiver costs or increasing worker productivity. That absent reasonable pricing investors won’t invest in this high-risk research that creates the new drugs. And they’re spending plenty on co-pay assistance programs (noting that insurers and PBMs don’t allow patients to sharing, through reduced co-pays, in the often-deep discounts pharmas give to payers).

But two kinds of pharmaceutical companies are trying a different approach: those developing biosimilars and at least one, EQRx, whose strategy focuses on charging radically lower prices for new and patented me-too brands. The boldness of biosimilar companies and a price-cutting start-up like EQRx lies precisely in the fact that they are directly trying to solve economic, not specifically clinical, problems.

But the ranks of these change agents should include more than the biosimilar manufacturers and EQRx’s of the world. Companies who see themselves entirely as research innovators should at least be considering cost-focused strategies because at least parts of their pipelines are often, despite the research investment, comparably undifferentiated. The specialty world is increasingly a me-too world – where for certain drugs the biggest opportunity may be as much in saving pharmaceutical costs as in trying to distinguish an at best incremental innovation for a skeptical payer audience of employers, state and federal governments, health plans, and patients.

The consequence of failing to create those cost-focused strategies, and a continuing increase in specialty-drug costs, may simply be the imposition of the easiest solutions: employer-empowered payers simply saying “no” – or, more dramatically, the meat cleaver of government intervention. That’s why it’s crucial for the entire pharmaceutical industry to understand the approaches and challenges of the most radical price-cutters.

Applying Generic Theory to Biologicals

First, some background. Specialty drugs drive most of the sector’s spending growth largely because that’s where the industry has poured its research energies. And for good reason: the problems are more obviously unsolved; the disease consequences are severe and symptomatic, so patients are more likely to seek treatment; development paths often shorter and thus cheaper than they are in primary care categories. And prices are higher than in primary care. Biologics are particularly attractive as specialty drugs since their patent lives are not as easily cut short by generics, as are small molecules.

Biosimilars could, theoretically, take a big bite out of the cost of those biologics which have lost exclusivity but nonetheless continue to sell at high WAC prices (an estimated $40 billion in US sales). In the US, however, they haven’t yet done so (with a few interesting exceptions which we’ll get to).

One main reason biosimilars haven’t done better is because they haven’t been allowed to. Innovators have planted thickets of patents around their products, extending exclusivity for decades. AbbVie has fended off biosimilar competition for years thanks to an impressive IP wall around Humira. Enbrel – launched 23 years ago – won’t see biosimilar competition till 2029.

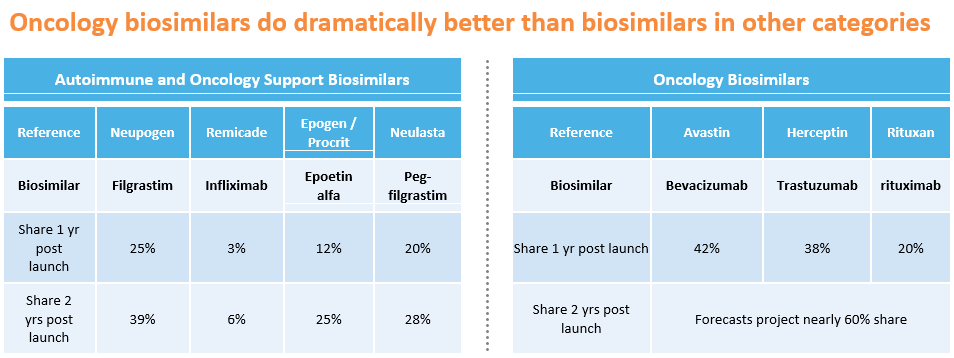

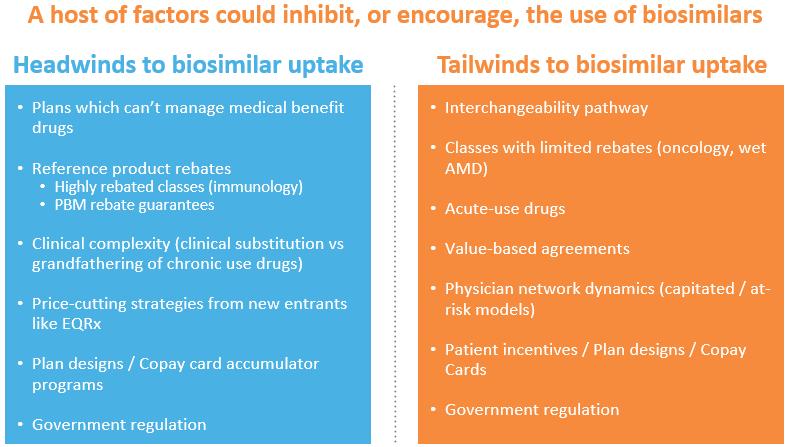

But there are plenty of other obstacles. Payers are often getting massive rebates from best-selling patent-expired biologics. Most of that rebate stream comes from scripts for existing patients – and it’s medically frowned upon to switch a patient benefiting from a biological to a competitor, including a biosimilar competitor. Since these rebate contracts often specify that the brand giving the rebate can’t be disadvantaged to any competitor, payers sensibly don’t force the issue. After all, a biosimilar priced 20% below the innovator’s WAC would have to generate a lot of market share to make up for lost rebate dollars from the market-dominating reference product. They wouldn’t only lose rebate dollars: payers and PBMs often guarantee their employer customers a minimum rebate volume. All of that is why biosimilars have taken only 6% of the Remicade market two years after they launched.

Where biosimilars might have a chance is in categories where the markets are large but rebating minimal – oncology, for example, or Wet age-related macular degeneration (Wet AMD). Oncology is particularly attractive: the therapy is generally acute, not chronic, so new patients constitute a much bigger user share than in immunological conditions like rheumatoid arthritis or psoriasis. That means patients don’t have to be switched off the innovator and re-started on the biosimilar. As importantly, rebates have been vanishingly small in oncology (as they have been in Wet AMD as well). Since they’re not forfeiting any significant rebate stream by doing so, payers can require patients to start therapy on the drug with the lowest net price – the biosimilar or a brand now willing to discount to maintain market share. One year after their launch, biosimilars have already taken 42% of Avastin’s market and 38% of Herceptin’s.

But if biosimilars do better in oncology than in immunology, they still don’t capture the majority of the market – certainly not the 90% share generics can get in small-molecule markets. The biggest problem is that they can’t afford to discount like generics can – and therefore can’t generally offer the lowest net price.

The basic issue is cost: they have development, manufacturing, and selling expenses more like brands than generics. Biosimilars are expensive to develop. A manufacturer first needs to design a protein that is, definitionally, “highly similar” to the originator and then prove it (a process that isn’t cheap). And the company then needs to make the protein, with yields and volumes big enough to keep costs as low as the originator’s. That originator is manufacturing large volumes and has presumably improved yields over time. Few biosimilar manufacturers have the yields and volumes to be able to compete with the costs of the originators. Samsung Bioepsis is probably one – but by and large they’re not in charge of selling their drugs in the US and their marketing partners (e.g. Biogen for biosimilar Lucentis and Eylea) have not historically competed on generic-style pricing. And finally, most biosimilars need sales forces (generics don’t) and have to provide the same kind of patient assistance programs the reference products do.

When Price is the Differentiator

Add up patents, high development and commercial costs, COGS, and rebates and that’s why another strategy is getting started: targeting biologics markets with new brands priced radically lower – maybe two-thirds lower — than the competitors’. At those kind of prices, even the rebate streams wouldn’t be enough to keep payers loyal to the originators. Moreover, a price-cutter could have a big portfolio advantage over the biosimilars: they can go after giant categories where no patents have expired – think multi-billion-dollar markets pioneered by the IL-17’s, IL-23’s, or the PD-1s.

Existing also-ran brands could do this today. But undercutting pricing in biologicals has been anathema to most manufacturers.

Newcomers might have fewer qualms. Or at least EQRx does. The company has convinced plenty of investors (it’s raised $750 million since its formation in 2019) and has built a portfolio of small- and large-molecule drugs, including a PD-1 and a PDL-1. From what one reads in the press, EQRx thinks it can develop these candidates as new brands – either me-toos or me-betters — and sell them for one-third the cost of the innovators’ drugs.

To do so, they have to keep their costs low. Presumably they’ve raised relatively low-cost capital, one assumes arguing to investors that development is far less risky because their candidates’ mechanisms of action have been proven and the regulatory paths well paved. One also must assume that portfolio costs are low because they’ve in-licensed their candidates, often from China, for modest prices. They thus wouldn’t have the same origination cost as the biosimilars (these are new molecules and so they don’t have the expense of proving they’re “highly similar”). Manufacturing costs are, for outsiders, an unanswered question.

There are, however, at least two structural disadvantages to a branded strategy like EQRx’s, and which are by and large not problems for the biosimilars.

The first stems from the fact that payers generally won’t cover a biologic that’s not approved for the prescribed indication. Humira is approved for 10 indications. Most are small, but a new competitor biologic would need to gain approval in the largest indications to displace it and its rebate stream. The biosimilar’s advantage, on the other hand, is that it is automatically approved for any indication its reference product is approved for – and thus starts out without the cost burden of multiple clinical trials. Oncology is easier: payers will cover a new drug as long as it’s got enough evidence to be listed in one of the accepted compendia, particularly NCCN. But getting that evidence still requires a trial.

An additional problem: a newcomer following the price-cutting strategy can most efficiently prove itself by trialing against placebo or a poor-performing older therapy – and in major markets, that no longer flies. Virtually all the new anti-inflammatories, for example, test themselves against the standard-of-care drugs, aiming for superiority and thus some kind of advantage. In oncology it’s even trickier: if a newcomer wants to test its PDL-1 for use in a big market, like non-small cell lung cancer (NSCLC), it probably has to test it against another PD1 (it’s unethical to use an inferior therapy as the control). Superiority will be tough to prove – and non-inferiority more expensive (non-inferiority trials generally require larger trial populations). Otherwise, the manufacturer has to find a unique, or nearly unique, indication, almost always very small market – which is exactly what virtually all PD-1 and PDL-1 competitors have done, including EQRx. It just announced a successful Chinese Phase III trial for its PDL-1, sugemalimab, in a heretofore un-trialed subset of NSCLC patients. But to be reimbursed in more common indications they’ll need clinical-trial evidence the drug works in them.

Another challenge for the new price cutters – and the biosimilar companies too — relates to a subset of biologicals, those which are physician administered. The biggest sellers, the oncologics and the macular degeneration drugs, represent huge shares of physician income thanks to the Rube Goldberg system of reimbursement called “buy-and-bill.” In that process, the physician buys the drug and then is allowed to charge a mark-up on the purchase, generally 4-6%. For the one-third of retina specialists who perform 80% of the macular degeneration injections, the markups on these drugs are paying the majority of their total compensation (which can be rich indeed). A similar story for oncologists for whom, likewise, buy-and-bill is a major part of their income. Most payers are loath to disrupt these economics for a variety of reasons – including the chance that some of those physicians will simply walk-away from their networks, leaving the insurer without the required medical coverage.

Insurmountable? No, But Hardly Straightforward

As we’ve outlined, the challenges these cost-focused players face are not insignificant. Mark Trusheim and Peter Bach think biosimilars’ challenges are so intractable that only price regulation can help. For any innovator biologic past its 12-year exclusivity date, they suggest a government-mandated fixed profit over production costs of 10-20%. Goodbye biosimilars.

Bach must be more sanguine about EQRx’s prospects: he is a co-founder. But that company and others who follow it also face impressive structural obstacles – not just the ones we’ve described above. The business model of the Big Three PBMs, which impact greater than 80% of industry prescribing, depends on rebates: they guarantee their payer and employer customers minimum rebates, which they must extract from manufacturers. But they get no benefit from buying a drug with a price as cheap as its net post-rebate price from its originator. And all the PBMs own expensively acquired specialty pharmacies – who, like buy-and-bill doctors, make more money from expensive drugs than from cheaper ones. Meanwhile, as health systems consolidate, they are increasingly addicted to buy-and-bill revenues.

Government could address all these structural impediments, and more. They could (and have tried to) abolish the current buy-and-bill system, giving providers a fixed-dollar markup for buying and administering a drug, not one based on a percentage of the price. They could (and have tried to) eliminate the rule that allows standard rebates a safe-harbor exemption from anti-kickback laws. The FDA could create a smoother and cheaper path to biosimilar “interchangeability” – allowing pharmacists to substitute the biosimilar for the brand, just as they can for generic small-molecule drugs. They could even pilot a biosimilars-style extrapolation policy for same-mechanism biologicals that have proven at least non-inferior to older drugs in major indications.

Or they could simply take out the governmental sword and slice the knot: set prices, one way or the other.

Any of these possibilities should be making the broader pharmaceutical industry think hard about the strategies and the goals of the price-cutters. Their aim, like generic companies before them, is to solve a pharmaceutical cost problem – a different healthcare problem than finding a new treatment, but certainly an important one. And it’s a goal that may be worth considering.

Indeed, many companies wouldn’t have to stretch far to see their own similarities to the price cutters. I don’t imagine, for example, when EQRx’s licensors began their R&D programs, that they thought of themselves as creating me-too’s. But they eventually recognized that that’s exactly what they’d done; that their drugs were not worth a premium price – and that their healthcare opportunity was cost savings, not unique therapies. There are many brand-name biopharmas in that same position: they simply haven’t realized it yet, although at least some of them have been quite specifically told. Ronny Gal, an analyst at Sanford Bernstein, has publicly called for Regeneron to lower the price of Libtayo – the most logical strategy, he thinks, to win market share for the sixth entrant in the PD-1/PD-L1 field. He goes further: to avoid government intervention in pricing, he writes, the best thing Regeneron “can do for the industry is to demonstrate that market forces work” – i.e., that competition drives down drug costs.

Whether brand-name companies can pursue two strategies at once — a cost-cutting strategy for part of their portfolios and an innovation strategy elsewhere — is uncertain. Many pharmas tried in the 1980s and 1990s to build generics operations – and all, with the single possible exception of Novartis with Sandoz, failed. Big Pharma couldn’t manage the speed and business requirements of a business with such tiny margins. But the pricing game in biologics will be very different – manufacturing and regulatory challenges will keep out generic-style competition.

A few companies have taken a step in this direction – Novartis’ Sandoz unit, along with Amgen, Pfizer, and Biogen, for example, all have biosimilar pipelines. Many other companies have what might be called virtual biosimilars or EQRx-style me-too’s – as Ronny Gal has suggested. Virtually none of them will make money – but they will continue to push up specialty drug spending.

Some of these companies could in fact blend innovation and economic strategies with value-based approaches. A new me-too brand, or a biosimilar, could start with a WAC price at a 20% discount to the market leader – and offer a value-based rebate based on performance. These contracts are increasingly straightforward to adjudicate through pharmacy and medical claims – there’s rarely a need for the kind of complexity that has scared off payers and manufacturers in the past.

Value-based approaches or other — if the industry is going to avoid sharp-edge government-imposed solution, they’d better start looking for other approaches to the healthcare cost problem. It’s therefore worth understanding what the price-cutters are up to – and up against.

[1] Business Group on Health – “2021 Large Employers’ Health Care Strategy and Plan Design Survey”